Key Takeaways

- The IRS considers all sports betting payouts as ordinary income, regardless of the amount or whether you received a tax form.

- For the 2026 tax year, you can only deduct 90% of your gambling losses against your winnings, even if you ended the year with a net loss.

- You must report the full win amount and itemize your deductions on Schedule A to claim any losses.

- Sportsbooks are legally required to report wins to the IRS via Form W-2G if you win $600+ at odds of 300:1 or greater.

- You are responsible for keeping a contemporaneous gambling diary and receipts to prove losses, as sportsbooks rarely provide IRS-ready loss documentation.

Whether you spent the year chasing longshot parlays or meticulously managing a bankroll, there’s one opponent you eventually have to face…

…The IRS.

And by understanding the intersection of sports betting and your taxes, you can stop guessing how much of your balance is actually yours and start using the tax code to protect your winnings.

So let’s talk about how to stay compliant and ensure that your victory doesn’t position you for a loss at tax time.

Do you have to pay taxes on sports betting?

The short answer: Yes, sports betting winnings are taxable income.

The IRS operates on the principle that everything you earn is taxable unless the tax code explicitly states otherwise.

Sports betting is not an exception. Whether it’s a small win on a weekend game that you and your Shakopee, MN fantasy football team sunk some money into or a major jackpot from that little trip to Vegas you did for work… your winnings are considered taxable income, just like capital gains on a stock or your annual salary.

It’s a common misconception that you only owe taxes if you receive a specific tax form (like a W-2G) or if you withdraw money from your sportsbook account.

In reality, you are legally required to report ALL gambling winnings as income on your federal tax return.

This requirement isn’t limited to just the NFL or NBA. It includes:

- Sports betting: Online apps, retail sportsbooks, and prop bets.

- Casino games: Slots, blackjack, and poker.

- Other luck-based wins: Lotteries, bingo, keno, and horse racing.

Does the IRS track sports betting?

Modern sportsbooks (especially digital platforms like DraftKings, FanDuel, and BetMGM) are highly regulated and maintain transparent paper trails for the federal government.

Here is how the tracking system works and what triggers a formal report to the IRS.

When you hit a payout that meets specific IRS criteria, the sportsbook is legally required to generate Form W-2G, Certain Gambling Winnings. One copy goes to you (by January 31, 2027), and the other goes directly to the IRS.

This form includes:

- Your total reportable winnings

- The date of the wager

- The type of gambling activity

- Any federal or state income tax withholding that was taken out upfront

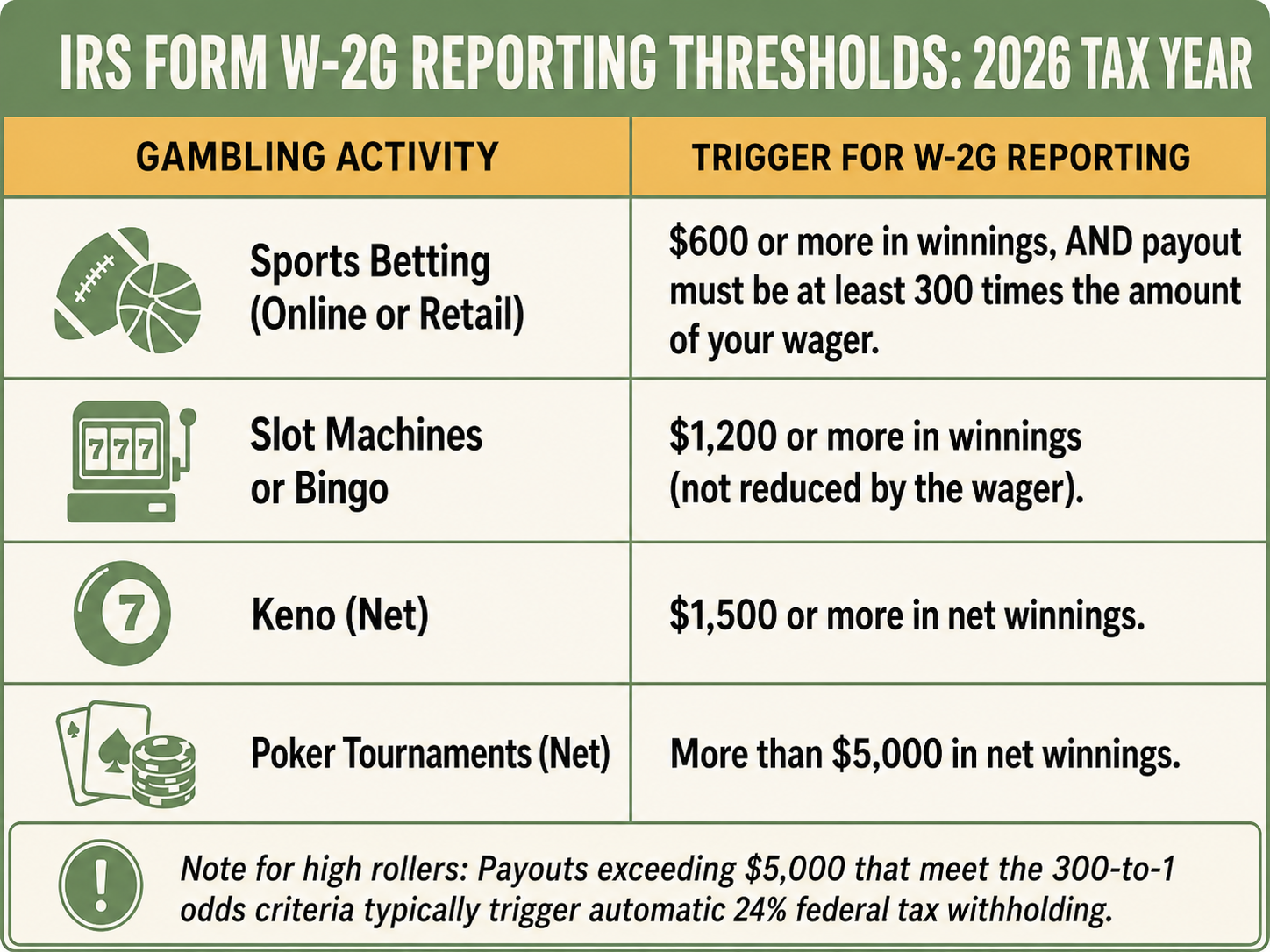

For the 2026 tax year, you should expect to receive a W-2G if your winnings meet any of the following benchmarks:

- You win $600 or more in sports betting, provided the payout is at least 300 times the amount of your wager.

- You win $1,200 or more in slots or bingo (not reduced by the wager).

- Your net Keno winnings are $1,500 or more.

- Your net poker tournament winnings exceed $5,000.

If you’re a high roller and win more than $5,000 on a wager that meets the 300-to-1 odds criteria, the sportsbook is typically required to automatically withhold 24% for federal taxes before they even pay you.

Do I have to report sports betting winnings if I don’t receive a W2-G?

Absolutely. The W-2G is a reporting requirement for the business, not a definition of taxability for you the individual.

Even if you won $400 on a game (below the $600 threshold) or $1,000 on a short-odds bet (not meeting the 300:1 rule), the IRS still considers that income. You won’t get a form, but you’re still legally obligated to self-report those wins on your return.

At the same time, the IRS recognizes that informal gambling exists. Your Scott County coworker running your $20 March Madness bracket pool isn’t going to send you a W-2G.

However, from a strict tax standpoint, those winnings are still technically reportable income. While the IRS may not have a digital trail for a cash-based office pool, being consistent with your reporting is the best way to protect yourself in the event of a broader financial audit.

Can you deduct gambling losses from your winnings?

You can deduct your gambling losses to offset your winnings, but under the new 2026 tax rules, you can no longer wash your wins entirely (even if you broke even).

Here are three things you need to know about the deduction process.

1. The 90% rule

In previous years, the IRS allowed you to deduct 100% of your gambling losses, provided they didn’t exceed your winnings. But because of the OBBBA, starting with the 2026 tax year, you can now only deduct 90% of your gambling losses against your winnings.

Imagine you bet $100 on 10 different NFL games throughout the season and lost all of them. (Total Loss: $1,000.) Then, you hit a big $1,000 win on the Super Bowl.

Under the new 2026 rule: $1,000 win – $900 (90% of your loss) = $100 taxable income. Even though you are down $0 for the year, you now owe income tax on that remaining $100.

2. The itemization challenge

To take advantage of this deduction, you must itemize your deductions on your tax return.

Taxpayers in the middle and lower income tax brackets don’t typically exceed the Standard Deduction limit ($16,100 for individuals in 2026), so itemizing won’t matter there.

However, if you do usually itemize, you cannot deduct any gambling losses. You will be taxed on the gross amount of your winnings, regardless of how much you lost.

3. Sportsbooks track wins

While your online sportsbook sends you a W-2G for a big win, they don’t provide the same level of IRS-ready documentation for your losses.

So, the burden of proof for your gambling losses is on you. You need to maintain a contemporaneous gambling diary that includes:

- The date and type of specific wagers.

- The name and location of the sportsbook or casino.

- Official receipts, tickets, or statements.

- A log of your actual sessions to substantiate the total amounts won and lost.

Final thoughts

The big takeaway here is that under the new 2026 rules, you can no longer assume that a break-even year is a tax-free year.

Because the OBBBA now limits your loss deductions to 90%, you may face an unexpected tax bill on phantom income even if you didn’t turn a profit.

So grab a time to chat with me. I’ll help you over this new math hurdle and ensure your record-keeping is robust enough to defend every dollar you’re entitled to keep.

FAQs

“How much do you pay in taxes if you win sports bets?”

In the eyes of the IRS, your sports betting winnings are treated as ordinary income. Which means they are taxed at the same marginal rate as the salary from your job. Depending on your total annual income (including your wages and your bets), your federal tax rate will fall into one of the seven tax brackets ranging from 10% to 37%.

“What happens if I win a bet in a state where I don’t live?”

If you place a winning bet while physically located in another state, you may owe non-resident state income taxes to that state. Most sportsbooks will track where the wager was placed, and you may receive a state-specific tax form. I can help you file the necessary non-resident returns and determine if your home state offers a credit to prevent you from being taxed twice on the same win.

“Do you have to pay taxes on sports betting for sportsbook promotions?”

Yes. The IRS generally views Bonus Bets, Site Credits, and promotional prizes as taxable income at their fair market value. For example, if you win a $500 bonus in a Refer-a-Friend promotion, that $500 is technically reportable income, even if you haven’t converted it to cash yet. These promos are often bundled into your year-end 1099 or W-2G totals.

“Do I have to pay self-employment tax on my sports betting winnings?”

For the vast majority of people, sports betting is a recreational activity, so you do not owe self-employment (Social Security and Medicare) taxes. However, if you are a professional gambler who pursues betting as a full-time trade or business, your net profits are subject to self-employment tax. Determining professional status is complex and depends on the frequency and business-like nature of your betting… something we should discuss in a consultation.

“Do you have to pay taxes on sports betting if you win a non-cash prize?”

The IRS requires you to report the Fair Market Value (FMV) of any physical prize as ordinary income. If you win a trip to the Super Bowl valued at $10,000, you must report that $10,000 on your return just as if you had won it in cash. Sportsbooks will typically issue a Form 1099-MISC for these types of high-value prizes.

“Can I use my sports betting losses to lower the taxes I owe on my regular job salary?”

No. Gambling loss deductions are strictly limited to the amount of your gambling winnings. You cannot use a bad year in sports betting to reduce the taxable income from your 9-to-5 paycheck or other investments. Under the 2026 rules, those losses are only useful for offsetting up to 90% of your reported betting wins for that specific tax year.